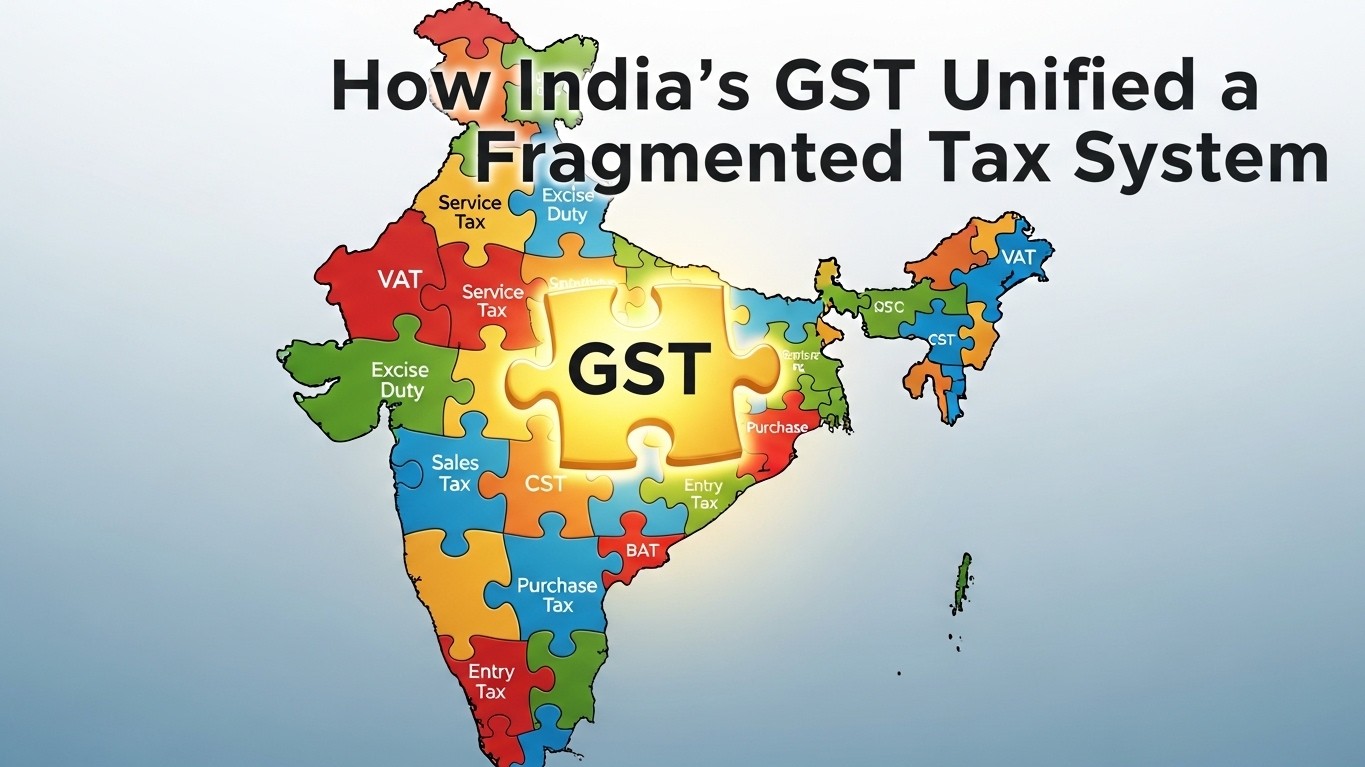

The Pre-GST Labyrinth: A Taxing Tale

So, In fact, Imagine a business owner in Mumbai wanting to sell goods in Delhi. Before 2017, this simple transaction triggered a cascade of taxes: Central Sales Tax (CST), state Value Added Tax (VAT), entry taxes. Also, more. Each state had its own tax laws, rates. Also, compliance procedures, creating a logistical nightmare and a significant cost burden. This fragmented tax structure not only hampered inter-state trade but also incentivized tax evasion and stunted economic growth. The pre-GST era was a labyrinth. Also, businesses were constantly trying to handle its complexities.

The Cascading Effect: Tax on Tax

You see, The most significant flaw of the old system was the 'cascading effect' of taxes. Tax was levied on the value of goods at each stage of production and distribution, without allowing credit for taxes already paid on inputs. This meant that the final consumer ended up paying tax on tax, inflating prices and making Indian goods less competitive in the global market. This cascading effect was like a chain reaction, each link adding to the final burden.

Inter-State Trade Barriers: A Patchwork Economy

You see, Each state acted as an independent tax jurisdiction, creating barriers to inter-state trade. Check posts at state borders caused delays and increased transportation costs. Businesses had to comply with different tax laws in each state where they operated, leading to increased compliance costs and administrative overhead. This patchwork economy stifled innovation and discouraged investment. It was like trying to run a marathon with hurdles every few meters.

The Vision for GST: A Unified Market

So, Here's the thing: The Goods and Services Tax (GST) was envisioned as a full, multi-stage, destination-based tax levied on every value addition. The core idea was to create a unified national market, eliminate the cascading effect of taxes. Also, simplify the tax system. This bold move aimed to boost economic growth, improve tax compliance. Also, make better India's competitiveness. GST was designed to be the key that unlocked India's economic potential.

Eliminating Cascading Taxes: A Simple Flow

You see, GST allows businesses to claim input tax credit (ITC) for taxes paid on inputs used in the production or provision of goods and services. This eliminates the cascading effect of taxes, reducing the all in all tax burden and making goods and services more affordable. ITC ensures that tax is only levied on the value added at each stage, creating a smooth flow of taxes from the manufacturer to the consumer. This is like replacing a leaky pipe with a smooth, efficient pipeline.

Creating a Common National Market: One Nation, One Tax

In fact, In fact, GST replaced multiple indirect taxes with a single tax, creating a common national market. This eliminated inter-state trade barriers, reduced transportation costs. Also, simplified compliance procedures. Businesses could now operate across state borders without having to worry about different tax laws and regulations. This is like removing the walls between different rooms to create a spacious, open plan living area.

Simplifying Tax Compliance: Ease of Doing Business

You see, GST introduced a simplified tax compliance system with online registration, filing of returns. Also, payment of taxes. This reduced the administrative burden on businesses and made it easier to comply with tax laws. The GST Network (GSTN) provides a common platform for all taxpayers, facilitating simple interaction with tax authorities. This is like upgrading from a manual typewriter to a modern computer with user-friendly software.

The Challenges GST Aimed to Deal with

The introduction of GST was not merely about simplifying taxes; it was a planned move to handle deep-rooted challenges in the Indian economy.

Tax Evasion: Plugging the Loopholes

Here's the thing: Here's the thing: The complex and fragmented tax system before GST made it easier for businesses to evade taxes. GST, with its emphasis on transparency and accountability, aimed to plug these loopholes. The input tax credit mechanism incentivizes businesses to declare their transactions and pay taxes, reducing the scope for tax evasion. This is like installing security cameras to deter theft.

Black Money: Promoting Transparency

You see, Here's the thing: The pre-GST era was characterized by a significant amount of black money circulating in the economy. GST, by promoting transparency and formalizing the economy, aimed to curb the generation and circulation of black money. The electronic tracking of transactions and the mandatory registration of businesses under GST made it more difficult to hide income and evade taxes. This is like shining a spotlight on hidden activities.

Boosting Economic Growth: A Catalyst for Progress

Here's the thing: You see, By creating a unified national market, eliminating the cascading effect of taxes. Also, simplifying tax compliance, GST aimed to boost economic growth. The reduced tax burden and increased efficiency were expected to stimulate investment, increase production. Also, create jobs. GST was envisioned as a catalyst for economic progress, driving India towards a brighter future. This is like adding fuel to a fire, igniting economic growth.

Conclusion: A Transformative Reform

Here's the thing: So, The introduction of GST was a landmark reform that transformed India's tax scene. While challenges remain, the benefits of GST are undeniable. It has created a unified national market, eliminated the cascading effect of taxes, simplified tax compliance. Also, boosted economic growth. GST is an ongoing journey. Also, continuous improvements are needed to realize its full potential. It's a proof to India's commitment to economic reform and its aspiration to become a global economic powerhouse. The move towards GST was not just a change in tax laws; it was a fundamental shift in India's economic philosophy.